The value of the US dollar will continue to be eroded by the continually escalating budget and trade deficits. The US government is spending far more each year that it receives in taxes and has little financial restraint. In addition, millions of baby boomers are getting ready to retire and are living longer, which will strain the US entitlement budget. The trade deficit is a huge threat to the dollar and US economy as all of the wealth in US gets exported abroad. At the same time, the oil exporting countries and China continue to aggregate wealth from the rest of the world.

I am currently reading Senator Byron Dorgan's book, Take This Job and Ship It, and he has a great passage in the first chapter stating that "American consumers watch our Japanese television set, wearing our Chinese T-shirts, Taiwanese trousers, Mexican shorts, and Italian shoes. We drive a Korean car to the store to pick up our Mexican vegetables, Australian beef, and a six-pack of Heineken. And then we wonder what happened to all of the good jobs here at home." If foreigners do not buy US goods and services at the same rate that US citizens purchase foreign goods, then US capital will slowly be eroded and disbursed to the rest of the world, ultimately reducing the value of the US dollar. The US dollar has already declined significantly compared to the Chinese Yuan, Euro, Pound, and Australian dollar over the last 5 years and this trend will most likely continue over the next decade.

Friday, December 29, 2006

Thursday, December 28, 2006

Hertz IPO Perfoms Better than Expected

Hertz Global, HTZ, is currently trading at $17 per share today on Dec. 28th, up more than 10% from the IPO price of $15 on Nov. 16th. Lehman Brothers released on Overweight rating on Hertz with a target price of $20 per share two days ago. Lehman cites the experienced management team, the low age of the car fleet relative to its competitors, the cost-cutting expertise of management and the 30% market share they have which towers over their competition. Their 22-page report also predicts robust margin and profit growth due to increased personal and business travel over the next few years. The Lehman reports makes a strong case that Hertz is the best run car rental firm in the world. However, what price is one willing to pay to own a piece of this company. Lehman optimistically predicts Hertz will earn profits of 79 cents per share in 2006 and 95 cents per share in 2007. These estimates far exceed the profit of 64 cents per share in 2006 and 65 cents per share in 2007 predicted o average by analyst submissions to Yahoo Finance. Even in the most optimistic case, the car rental business is a very competitive business and I would not pay more than 14x 2007 earnings estimates for a share of this company which equals $13.3 per share, making HTX overvalued by over 20%. Time will tell whether the auto rental industry is as strong as Lehman anticipates or less robust as I anticipate.

Megatrend #3: Healthcare will continue to grow

As the world population continues to increase in age and lifespan, healthcare will continue to grow and be an increasing share of the world economy. Drug spending is rising at double digits per year. Companies that specialize in acute care and homecare are continuing to grow and the need for physicians in the US continues to outpace demand. Surgery for hips, knees, backs, and hearts are also rising as an aging population demands to be as active as when they were younger. Cosmetic surgery is also in high demand as the old insist on looking and feeling much younger. Billions are being spent currently on genetic and stem cell research for future drugs as well. Healthcare is continuing to be a growing part of the global economy.

Beware of Real Estate Carrying Costs

Many people that are actively looking for a new home focus on the purchase price and monthly payment based on current interest rates in order to determine whether they can afford a new home. However, there are many additional costs that have become more significant that one needs to be more cognizant of these days. These costs include: maintenance costs, real estate taxes, insurance, and electricity/heating/cooling costs.

Maintenance costs usually run about 1% of the price of a new home each year. These costs include general maintenance and upkeep to a home. On a $400,000 house, these costs will average about $4,000 per year.

Real estate taxes have been increasing at a rapid rate across the country over the last 5 years. The average homeowner in the Washington, DC metro area current pays over $4,000 per year in real estate taxes and these taxes are climbing at 10% per year.

Home insurance has tripled in cost over the last 5 years due to storms and high claims. I blame much of the increase on global warming causing more severe storms as well as shoddy construction of new homes. Have you seen a new home built recently by a national builder? These new homes go up in less than a month and have the cheapest structure and siding I have ever seen. I believe that many of these homes were designed to crumble to the grund once their 30 year mortgages have been paid off. One should budget at least $800 per year for home insurance.

Energy costs have also been escalating at a rapid rate with natural gas and heating oil costs soaring and electricity rates set to double in areas such as Washington, DC. One should budget at least $250 per month for all electricity/heating/cooling.

Let's add up the additional carrying costs for a home that we have calculated so far:

$4,000 per year home maintenance

$4,500 per year real estate taxes

$900 per year home insurance

$3000 per year electricity/heating/cooling

Grand total: $12,400 = $1,033 per month.

Over $1,000 per month needs to be budgeted for home carrying costs.

It is important for new home owners to keep this in mind in the purchase process.

Maintenance costs usually run about 1% of the price of a new home each year. These costs include general maintenance and upkeep to a home. On a $400,000 house, these costs will average about $4,000 per year.

Real estate taxes have been increasing at a rapid rate across the country over the last 5 years. The average homeowner in the Washington, DC metro area current pays over $4,000 per year in real estate taxes and these taxes are climbing at 10% per year.

Home insurance has tripled in cost over the last 5 years due to storms and high claims. I blame much of the increase on global warming causing more severe storms as well as shoddy construction of new homes. Have you seen a new home built recently by a national builder? These new homes go up in less than a month and have the cheapest structure and siding I have ever seen. I believe that many of these homes were designed to crumble to the grund once their 30 year mortgages have been paid off. One should budget at least $800 per year for home insurance.

Energy costs have also been escalating at a rapid rate with natural gas and heating oil costs soaring and electricity rates set to double in areas such as Washington, DC. One should budget at least $250 per month for all electricity/heating/cooling.

Let's add up the additional carrying costs for a home that we have calculated so far:

$4,000 per year home maintenance

$4,500 per year real estate taxes

$900 per year home insurance

$3000 per year electricity/heating/cooling

Grand total: $12,400 = $1,033 per month.

Over $1,000 per month needs to be budgeted for home carrying costs.

It is important for new home owners to keep this in mind in the purchase process.

2007 - The Year for Mortgage ARM Resets

Over $1 Trillion of mortgage debt is set to reset in 2007 causing many homeowners lots of pain and increases in payments and possibly foreclosure. The belief in the financial markets recently is that the housing market has bottomed and that housing will stabilize in 2007 since ne home sales in November were relatively strong and home inventory for sale has been gradually declining. However, the mortgage debt ready to reset will impact the housing market mext year, keeping things weak. In addition, the strong new housing data has been more of a reflection of builders cutting prices to move inventory and not a core increase in consumer demand. Home inventory levels have also been dropping because there are few buyers out and about in the wintertime and many people are not interested in keeping an active listing for their home if there are few buyers out there shopping. The spring and summer of 2007 will be true test of the strength of the US home market, but if you are in the market for a new home, do not rush and look for the right home at the right price.

Is the Roth 401K for me?

Over the last couple of weeks, I have had a lot of people ask me whether the Roth 401K is appropriate for them. The answer is that it depends on the individual. If one believes that tax rates in the future will be the same or higher than today, then the Roth 401k is worth consideration. However, many people I know are currently in a high tax bracket and paying high income taxes in states such as Washington DC, Maryland, and Virginia. In this circumstance, one may be better off defering taxes to retirement when one may be in a lower tax bracket and possibly retired to a no icome tax state such as Florida.

Also, many people I know are exposed to paying the Alternative Minimum Tax (AMT). tax-deferred 401k contributions help to lower one's overall take home pay, thus limiting their exposure to paying AMT.

People have also asked me about the matching 401k contributions that employers provide. Is there a benefit to having the employer contributions matched into a Roth 401k plan versus a standard 401k? Unfortunately the majority of employers will only match contributions on a pre-tax basis. This complicates matching contributions in a Roth 401k, because one may have tax-free and tax-deferred money in a Roth 401k due to employer contributions that were not taxed. This complicates the process of figuring out tax owed once withdrawals are made.

Check with your financial advisor to determine if the Roth 401k is right for you.

Also, many people I know are exposed to paying the Alternative Minimum Tax (AMT). tax-deferred 401k contributions help to lower one's overall take home pay, thus limiting their exposure to paying AMT.

People have also asked me about the matching 401k contributions that employers provide. Is there a benefit to having the employer contributions matched into a Roth 401k plan versus a standard 401k? Unfortunately the majority of employers will only match contributions on a pre-tax basis. This complicates matching contributions in a Roth 401k, because one may have tax-free and tax-deferred money in a Roth 401k due to employer contributions that were not taxed. This complicates the process of figuring out tax owed once withdrawals are made.

Check with your financial advisor to determine if the Roth 401k is right for you.

Friday, December 15, 2006

Megatrend #2: Foreign markets will grow faster than the US

The economies of the emerging markets including Brazil, Russia, India, and China are growing at a faster pace than the United States creating investment opportunities in emerging markets. In addition, the US consumer is loaded with debt due to low interest rates and a high cost of living and the US government is loaded with debt. The interest payments on all of this existing debt limits the ability of the US to grow its economy at a faster rate than economies with less debt. The US also has a large trade imbalance with the rest of the world which means that US dollars are leaving the US for other parts of the world, also reducing US growth when those dollars are not reinvested back into the US economy.

Megatrend #1: Global Increase in Energy Demand

Currently, the 300 million people in the US, use over 1/3 of the global energy produced. Demand from emerging markets such as BRIC (Brazil, Russia, India, and China) continues to increase at double digits. Yet the global supply of energy continues to grow at a slower pace than demand and exploration and drilling costs continue to increase rapidly to bring new supply on the market.

The net result is that global energy prices will continue to increase for the forseeable future.

Integrated oil, natural gas. and coal companies, refiners, drillers, and equipment suppliers are all great ways to play this trend.

The net result is that global energy prices will continue to increase for the forseeable future.

Integrated oil, natural gas. and coal companies, refiners, drillers, and equipment suppliers are all great ways to play this trend.

Economy looking better..is it temporary?

This week retail sales for November were announced up 1.0% versus laster year, higher than expectations of .1% and jobless claims also came in weaker, driving the 10-year treasury bond yield back up to 4.6%. In addition, hiring is very strong in the services sector especially for skilled personnel, adding weight to the argument that the US economy is humming along nicely.

Is the optimism temporary, and just a part of the holiday season?

Hard telling I admit. I think the US economy will continue to experience hot spots and cold spots will an overall economy growing slower than the rest of the world.

Is the optimism temporary, and just a part of the holiday season?

Hard telling I admit. I think the US economy will continue to experience hot spots and cold spots will an overall economy growing slower than the rest of the world.

Friday, December 01, 2006

Further Proof of Slowing US economy

We had weak U.S. economic data released this week. Industrial activity is weakening fast and retail sales for November were mediocre expect at high-end and specialty retailers. In addition, consumer confidence dipped below the previous month and jobless claims were higher than Wall Street expected. The 10-year bond fell to an interest rate of 4.425% this year, a level not seen since January.

The action in the market definitely looks like one in which strength over the next month will be in healthcare, drugs, and food as people seek safety stocks in uncertainty about how bad of a recession we are going to get over the next year. Also these sectors are finally coming back after hitting recent lows a few days ago.

In addition, the survey of bulls versus bears continues to remain skewed towards a high level of optimism which is not good for further advances in the market anytime soon.

The action in the market definitely looks like one in which strength over the next month will be in healthcare, drugs, and food as people seek safety stocks in uncertainty about how bad of a recession we are going to get over the next year. Also these sectors are finally coming back after hitting recent lows a few days ago.

In addition, the survey of bulls versus bears continues to remain skewed towards a high level of optimism which is not good for further advances in the market anytime soon.

Friday, November 24, 2006

An Inconvenient Truth

Yesterday my family watched the movie created by Al Gore, An Inconvenient Truth. The movie was highly educational and informative, providing good evidence for global warming and the increased CO2 levels that humans are continuing to spew into the atmosphere. The movie helped to highlight several megatrends:

- Clean water will be a problem in the future as global warming dries up freshwater lakes, rivers, and mountain glaciers and we reach the limit in tapping fresh water from underneath the ground.

- Energy demands globally are continuing to increase each year, especially in the developing world. To exacerbate the situation, the US has spews 1/3 of the world's greenhouse gases and has done very little to slow the growth in CO2.

- Increased flooding and droughts will occur. This has been validated by the record huricane season in 2005 and also by my experience living on a farm in Maryland. Most recently on our farm we have experienced several month intervals with no precipitation at all during the fall and winter of 2006 and other months with record precipitation such as June 2006 and October 2006. The extremes seem to be a lot more common these days.

- Trees and forests are becoming more critical to the environment to help convert the CO2 in our atmosphere to oxygen and slowing the build up of greenhouse gases in our atmosphere.

So how do we take advantage of these megatrends from a financial and investment perspective?

To be continued...

Inflation or Deflation?

On Friday, US markets closed early at 1 pm instead of 4 pm, making for what should have been a dull day. However, the day was not dull at all:

- The US dollar fell to 19 month lows today against the Euro and has fallen to near record low levels against the Pound and Chinese Yuan recently.

- In addition, the US 10-year treasury bond receded below 4.55% today down to 4.548%. The 10-year bond has not been this low since January 2006.

- Gold also climber to $637.90, within $30 of its record high

- Oil prices also climbed today above $60 per barrel, which would be expected given global growth in energy demand, except for the fact that US inventories of oil are much higher than last year at this time.

Other data that came out this week include the fact that:

- Employee wages as reported by the government are soaring, up 5% year over year. I would not have believed this statistic given the lack of raises in much of corporate America these days. However, a coworker of mine, recently left our telecom company and she is getting a signing bonus plus a big raise to take another offer.

- Discounts at retailers are extremely aggressive this season with Wal-Mart continuing to lower prices on electronics, toys, and food.

What can we make of all of this data?

Inflationary signals: Dollar falling, Commodities rising, Wages rising.

Deflationary signals: 10-year treasury bond interest rate, retailers dropping prices.

Conclusion:

- The US economy is slowing due to slowing real estate prices, slowing car purchases, and slowing retail purchases.

- Inflation will be muted even though commodities are increasing in demand and price worldwide. This is due to the fact that the US economy has become more of a services economy and less of a commodity based economy.

- Those who are highly-skilled will continue to be in high demand and will be able to charge a premium for their services in today's global economy, thus continuing the paradigm shift of making some folks in the US economy very successful and wealthly while at the same time others are struggling. This conclusion is reinforced by the record bonuses to be given out on Wall Street this year.

So how do we invest successfully in an environment where the US economy is slowing, but the rich continue to do well? I will be discussing several mega-trends and themes for investing over the course of the next month.

Friday, November 17, 2006

US Economy slowing

Today, US housing construction fell to its lowest level in 6 years. Housing has been one of the major drivers of growth in the US economy over the last 5 years. The Consumer Price Index (CPI) reported yesterday also fell last month for the second straight month. Combined with oil prices diving to $55 per barrel this morning and other commodity prices in slow decline, I believe the US economy is headed into a period of very low inflation or deflation from a period of higher than average inflation. The REITs and utility averages where high-dividends rule are close to new highs which help confirm the low interest rate and inflation period that we are heading towards next year.

Hertz IPO is a bust

The Hertz Global (HTZ) IPO went off yesterday at $15 per share, lower than the anticipated $16-$18 per share planned price. People are having a harder time justifying the nose-bleed valuations for these Private Equity offerings. The stock closed yesterday at around $15.72. I anticipate that Hertz will move lower than the IPO price over the next couple of months.

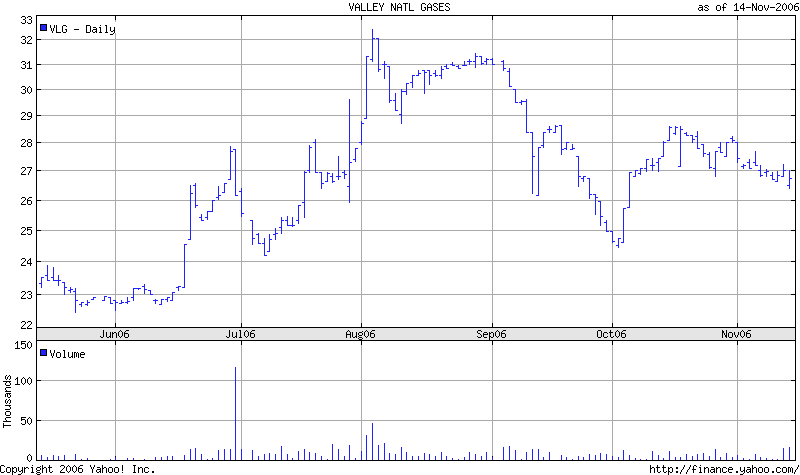

Tuesday, November 14, 2006

Another buyout of a company I own :(

Whenever you hear the news that a company whose shares you own are being bought out and taken private, you usually jump for joy. Not in this case however.

From bizjournals.com:

Valley National Gases (AMEX:VLG - News) is a supplier of industrial, medical and specialty gases and related equipment and is based in Washington, Pa.

Caxton-Iseman Capital, the New York investment firm, is acquiring Valley National's outstanding shares for about $249 million, and assuming the company's debt for a total transaction value of about $312 million.

Under the terms of the agreement, Valley National shareholders will receive $27 in cash for each share they own, which is equal to Monday's closing price.

Valley National will continue to be based in Washington, Pa., but will now operate as a private company.

"We are investing because we believe Valley National is well positioned to expand in its existing markets and enter new geographies through strategic acquisitions and internal growth," said Caxton-Iseman managing partner Frederick Iseman.

----

Valley National is being purchased without any premium provided to shareholders. To add insult to injury, as you can see by the chart, VLG has traded $5 higher in the last 6 months. In fact I actually sold half of my stake at $32 this summer because it had more than doubled from my originial purchase price. However, I never would have expected an investment firm to be able to purchase the company at only $27 per share. What a steal! The press release even admits that the company is well positioned for growth.

We can only hope that a secondary suitor comes within the next few weeks to outbid Caxton-Iseman Capital. Two years ago, I owned an oil tanker firm, Stelmar Shipping that received a buyout from another tanker firm. The final buyout price ended up being almost $10 more than the original buyout offer due to disgrunted shareholders unwilling to tender their shares to management. Unfortunately in this case, insiders own the majority of the shares, so we minority shareholders may be screwed. Oh well. I still cannot complain too much on a company who shares have doubled in the last 18 months.

{kind=link}

From bizjournals.com:

Valley National Gases (AMEX:VLG - News) is a supplier of industrial, medical and specialty gases and related equipment and is based in Washington, Pa.

Caxton-Iseman Capital, the New York investment firm, is acquiring Valley National's outstanding shares for about $249 million, and assuming the company's debt for a total transaction value of about $312 million.

Under the terms of the agreement, Valley National shareholders will receive $27 in cash for each share they own, which is equal to Monday's closing price.

Valley National will continue to be based in Washington, Pa., but will now operate as a private company.

"We are investing because we believe Valley National is well positioned to expand in its existing markets and enter new geographies through strategic acquisitions and internal growth," said Caxton-Iseman managing partner Frederick Iseman.

----

Valley National is being purchased without any premium provided to shareholders. To add insult to injury, as you can see by the chart, VLG has traded $5 higher in the last 6 months. In fact I actually sold half of my stake at $32 this summer because it had more than doubled from my originial purchase price. However, I never would have expected an investment firm to be able to purchase the company at only $27 per share. What a steal! The press release even admits that the company is well positioned for growth.

We can only hope that a secondary suitor comes within the next few weeks to outbid Caxton-Iseman Capital. Two years ago, I owned an oil tanker firm, Stelmar Shipping that received a buyout from another tanker firm. The final buyout price ended up being almost $10 more than the original buyout offer due to disgrunted shareholders unwilling to tender their shares to management. Unfortunately in this case, insiders own the majority of the shares, so we minority shareholders may be screwed. Oh well. I still cannot complain too much on a company who shares have doubled in the last 18 months.

Flip This Company

The Washington Post this morning had a good article on the coming IPO for Hertz Global Holdings, the largest car rental company in the world. Less than a year ago, three investment firms bought Hertz from Ford Motor Co. for $15 Billion, putting up $2.3 Billion of their own money and then loading up Hertz with more than $12 Billion in debt.

Now it gets more interesting. The three investment firms recently paid themselves a $1 Billion dividend and plan to pay themselves an additional $400 Million upon completion of a soon to be completed Initial Public Offering (IPO). After the IPO, the three firms will still control 72% of Hertz, which would be valued at $18 Billion including $12 Billion in debt.

Let’s do the math: the investment firms put down $2.3 Billion, 15.33% of the purchase price into Hertz. In less than a year, the investment firms will have paid themselves $1.4 Billion and will still control 72% of Hertz’s equity of $6 Billion equal to $4.3 Billion. In less than a year, the $2.3 Billion investment will have turned into $5.7 Billion or a return of 148%.

No wonder private equity firms are so hot and the graduates of the Wharton School MBA program are clamoring to work for private equity investment firms.

Lets ask and try and answer a few questions here:

1. Did Ford undervalue Hertz when it sold it to the 3 investment firms?

Based on the S-1 filing for the Hertz IPO, we see that earnings for Hertz were $158.6 Million is 2003, $365.7 Million in 2004, and $371.3 Million in 2005 through December 20th. If we round up to $375 Million for earnings in 2005 and divide the purchase price of $12 Billion by $375 Million, we get a Price to Earnings (P/E) ratio for Hertz in 2005 of 32. The valuation based on P/E appears to be high based on revenue growth of 8-10% per year. At first glance it certainly does not look like Ford undervalued Hertz.

2. How does the valuation of Hertz compare to its publicly traded competitor Avis Group?

Let’s take a look at Price to Sales. Price to Sales upon completion of the buyout was $12 Billion divided by $7.5 Billion in 2005 which equals 1.6. Avis Group is trading at only .11 times sales and is valued at $2 Billion versus the planned $18 Billion for Hertz.

What are we missing here?

Per the company description, Avis has approximately 6,600 car and truck locations in North America, Australia, New Zealand, Latin America, and the Caribbean.

Hertz, on the other hand, has approximately 7,600 locations in approximately 145 countries. Does having 1,000 more rental locations around the world equal 9 times the market capitalization?

Also, Avis is burdened with a substantial amount of debt just like Hertz will be after the IPO.

Hertz’s valuation after the IPO will look like a pig with lipstick in comparison to Avis.

3. What changed at Hertz to make the company worth 50% more in less than a year?

Good question. I haven’t figured out the answer yet to that given what I have read so far concerning the valuation and risks for Hertz.

4. Have the investment firms overloaded Hertz with too much debt?

Pretty close. As the S-1 states “We are highly leveraged and a substantial portion of our liquidity needs arise from debt service on indebtedness incurred in connection with the Transactions and from the funding of our costs of operations, working capital and capital expenditures.”

5. Does a firm that is burdened with a ton of debt justify such a high valuation?

The market values stocks per supply and demand in the marketplace. I am interested to find out who is buying shares of the Hertz IPO in order to justify the valuation.

To be continued...

Now it gets more interesting. The three investment firms recently paid themselves a $1 Billion dividend and plan to pay themselves an additional $400 Million upon completion of a soon to be completed Initial Public Offering (IPO). After the IPO, the three firms will still control 72% of Hertz, which would be valued at $18 Billion including $12 Billion in debt.

Let’s do the math: the investment firms put down $2.3 Billion, 15.33% of the purchase price into Hertz. In less than a year, the investment firms will have paid themselves $1.4 Billion and will still control 72% of Hertz’s equity of $6 Billion equal to $4.3 Billion. In less than a year, the $2.3 Billion investment will have turned into $5.7 Billion or a return of 148%.

No wonder private equity firms are so hot and the graduates of the Wharton School MBA program are clamoring to work for private equity investment firms.

Lets ask and try and answer a few questions here:

1. Did Ford undervalue Hertz when it sold it to the 3 investment firms?

Based on the S-1 filing for the Hertz IPO, we see that earnings for Hertz were $158.6 Million is 2003, $365.7 Million in 2004, and $371.3 Million in 2005 through December 20th. If we round up to $375 Million for earnings in 2005 and divide the purchase price of $12 Billion by $375 Million, we get a Price to Earnings (P/E) ratio for Hertz in 2005 of 32. The valuation based on P/E appears to be high based on revenue growth of 8-10% per year. At first glance it certainly does not look like Ford undervalued Hertz.

2. How does the valuation of Hertz compare to its publicly traded competitor Avis Group?

Let’s take a look at Price to Sales. Price to Sales upon completion of the buyout was $12 Billion divided by $7.5 Billion in 2005 which equals 1.6. Avis Group is trading at only .11 times sales and is valued at $2 Billion versus the planned $18 Billion for Hertz.

What are we missing here?

Per the company description, Avis has approximately 6,600 car and truck locations in North America, Australia, New Zealand, Latin America, and the Caribbean.

Hertz, on the other hand, has approximately 7,600 locations in approximately 145 countries. Does having 1,000 more rental locations around the world equal 9 times the market capitalization?

Also, Avis is burdened with a substantial amount of debt just like Hertz will be after the IPO.

Hertz’s valuation after the IPO will look like a pig with lipstick in comparison to Avis.

3. What changed at Hertz to make the company worth 50% more in less than a year?

Good question. I haven’t figured out the answer yet to that given what I have read so far concerning the valuation and risks for Hertz.

4. Have the investment firms overloaded Hertz with too much debt?

Pretty close. As the S-1 states “We are highly leveraged and a substantial portion of our liquidity needs arise from debt service on indebtedness incurred in connection with the Transactions and from the funding of our costs of operations, working capital and capital expenditures.”

5. Does a firm that is burdened with a ton of debt justify such a high valuation?

The market values stocks per supply and demand in the marketplace. I am interested to find out who is buying shares of the Hertz IPO in order to justify the valuation.

To be continued...

Subscribe to:

Posts (Atom)